The white metal’s psychological ceiling is still too rich for our blood.

While silver has continued its uptrend in the face of materially hawkish data, its inability to consistently hold $24 highlights its fundamental frailty. Moreover, while the recent weakness is immaterial, given how overvalued the price is relative to the fundamental backdrop, a substantial drawdown should occur over the medium term.

While the crowd doesn’t care at the moment, Fed officials have furiously pushed back against investors’ pivot hopes; and from our perspective, these warnings are like a fire alarm that shouldn’t be dismissed.

For example, while market participants have become more brazen in their condescending attitudes toward the FOMC’s projections, officials have equally upped the ante. Before, Fed officials used hawkish, but passive, language to avoid upsetting investors. Now, they’re being much more direct.

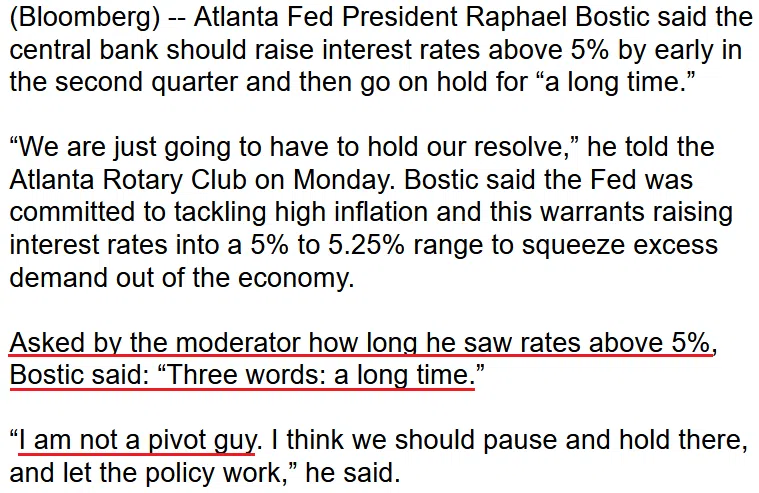

Atlanta Fed President Raphael Bostic said on Jan. 9:

Source: Bloomberg

Source: Bloomberg

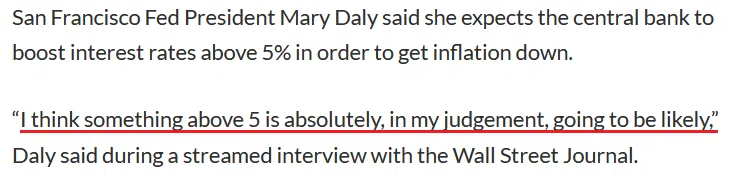

Likewise, San Francisco Fed President Mary Daly said on Jan. 9:

It is “really too soon to declare victory” on inflation. “We’re determined, dedicated, united, resolute… to bringing inflation down to our price stability target,” and we’ll keep at it “until the job is well and truly done.”

As a result, Daly also expects the FFR to exceed 5% in 2023.

Please see below:

Source: MarketWatch

Source: MarketWatch

Thus, while the PMs continue to call the Fed’s bluff, investors are not prepared for a Fed that actually delivers on its promises; and since the 2022 divergences ended with risk assets suffering sharp drawdowns, we believe they are more relevant than the post-GFC crowd’s prayers for QE.

In addition, the New York Fed released its Survey of Consumer Expectations (SCE) on Jan. 9; and while short-term inflation expectations fell and long-term inflation expectations rose, the implications of widespread wage inflation were prevalent. The report stated:

“The median expected growth in household income rose by 0.1 percentage point to 4.6% in December, a new series high.”

Please see below:

To explain, the red line above tracks American households’ median 12-month income growth expectations, while the blue line above tracks Americans’ median 12-month earnings expectations. If you analyze the performance of the former, you can see that it hit a new all-time high. Similarly, the blue line jumped in December and matched its all-time high.

As a result, we’ve warned repeatedly that U.S. households are flush with cash, and persistent wage inflation only enhances consumers’ spending power.

On top of that, while the crowd assumed that higher interest rates would create a deluge of delinquencies, Americans are not concerned about their debt payments.

Please see below:

To explain, the mean probability of missing a debt payment declined again in December, and the metric currently stands near the low end of its pre-pandemic range. Therefore, while interest rates are much higher now, the developments have not stressed consumers to the point where demand destruction has materialized.

As such, Americans’ ability and willingness to spend should keep inflation uplifted for longer than the consensus expects, and a realization is bullish for the FFR, real yields and the USD Index.

Finally, former Fed Chairman Alan Greenspan warned on Jan. 3 that wage growth is too high to meaningfully reduce inflation without a recession. He said:

“We may have a brief period of calm on the inflation front but I think it will be too little too late.” If the Fed pivots, inflation “could flare up again and we would be back at square one. For that reason alone, I do not expect the Federal Reserve to loosen prematurely unless they deem it absolutely necessary, for example, to prevent financial market malfunctioning.”

Thus, while we warned on numerous occasions that it would take a climactic event (bank failure, labor market collapse, bankruptcy shock, etc.) to provoke a dovish 180, the resilient economic backdrop does not support that right now. As it stands, the FFR should continue its ascent, and the hawks should emerge victorious in the months ahead.

Overall, the silver price has consolidated recently and underperformed gold. But, both are trading well above their fundamental values, and their optimism is driven by investors’ misguided pivot expectations. As a result, when those hopes reverse, the silver price should follow suit. Consequently, while the S&P 500 has made some bullish advances, the outlook for risk assets remains bearish.

Please share your thoughts. Why is the economic data so resilient despite all of the doomsday predictions? Can it last? And who will blink first: investors or the Fed?

Alex Demolitor

Precious Metals Strategist