The CPI release may decide if silver’s daily weakness is temporary or a new trend.

With the silver price struggling to eclipse $24, sellers have emerged when the white metal nears the psychological level; and while today’s CPI print could amplify the volatility, the medium-term backdrop is bearish, not bullish.

For example, sticky inflation supports higher interest rates and a stronger USD Index . Moreover, we’ve noted previously that the Bank of Canada (BoC) and the Fed often mirror each other’s monetary policy due to their region’s geographical proximity and trade relationship.

Therefore, after the BoC raised its overnight lending rate by 50 basis points on Dec. 7 and hinted at a pause, we wrote on Dec. 8 :

While the BoC cited “excess demand” and “unemployment near historic lows,” and in the next breath, questioned “whether the policy interest rate needs to rise further,” the contradiction highlights the conundrum confronting North American central banks. With some areas of their economies running too hot, while others are too cold, they want to have their cake and eat it too.

However, the reality is that supporting growth encourages inflation, and history shows the gambit ends in a recession regardless of what they do; and while the BoC (and maybe the Fed next week) thinks the overnight lending rate could peak at 4.25%, we believe the central bank materially underestimates the challenges that lie ahead.

Yet, with BoC Governor Tiff Macklem (Canada’s Jerome Powell) sounding much different on Dec. 12, the about-face highlights the anxiety confronting North American central banks. In a nutshell: because they know about the difficulty of normalizing unanchored inflation, all that’s left is hope. He said:

“We are trying to balance the risks of over and under-tightening monetary policy. If we raise rates too much, we could drive the economy into an unnecessarily painful recession and undershoot the inflation target. If we don't raise them enough, inflation will remain elevated, and households and business will come to expect persistently high inflation.

“With inflation running well above target, this is the greater risk.”

Thus, while market participants have full faith in their central banks, they don’t realize that Powell and Macklem are driving blind. Not only were they woefully wrong about “transitory” inflation in 2021, but history shows they won’t pull off soft landings either.

As such, while Macklem admitted what we already knew, don’t be surprised if interest rates rise more than the consensus expects and economic growth is a major casualty.

Please see below:

Source: Global News

Source: Global News

On top of that, we warned throughout 2021 and 2022 that demand was the primary driver of high inflation, and even as supply chains normalize, the pricing pressures will continue. But, the New York Fed released its Survey of Consumer Expectations (SCE) on Dec. 12, and the report stated:

“Median inflation expectations decreased at both the one and three-year-ahead horizons in November, by 0.7 percentage point (to 5.2%) and by 0.1 percentage point, to 3.0%, respectively.”

So, problem solved, right?

Well, the report added:

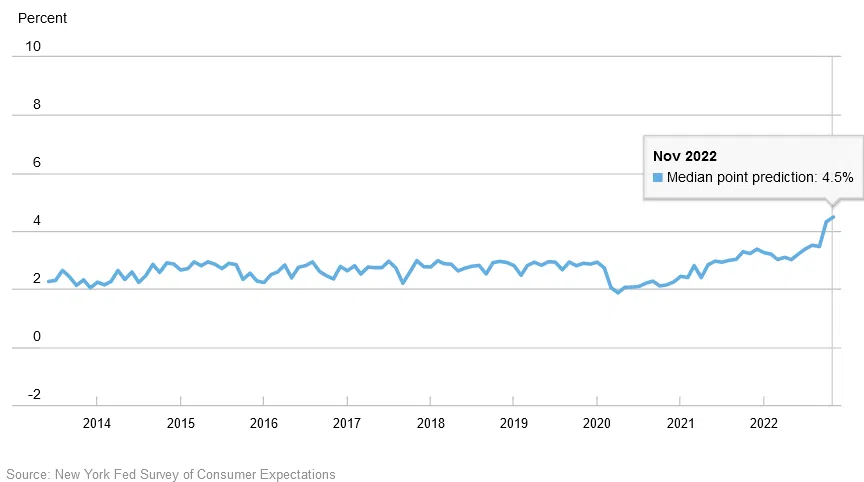

“The median expected growth in household income increased by 0.2 percentage point to 4.5% in November, a new series high.”

Please see below:

On top of that:

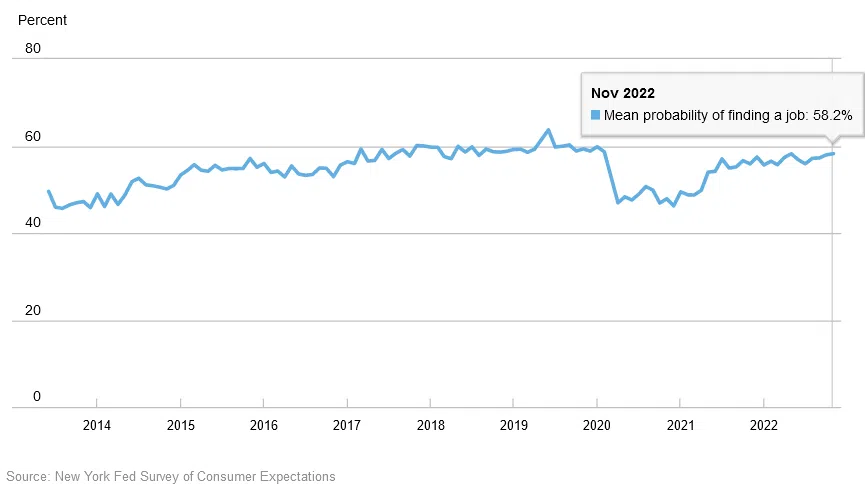

“The mean perceived probability of finding a job (if one’s current job was lost) increased by 0.2 percentage point to 58.2%, its fourth consecutive monthly increase and the highest reading since February 2020.”

Please see below:

Thus, with Americans expecting higher household income and more confidence in the U.S. labor market, demand should keep inflation elevated for much longer than the consensus expects. This means the fundamental backdrop is bullish for the FFR, real yields and the USD Index, and bearish for silver.

As further evidence, we warned on Dec. 23, 2021, that the crowd underestimated Americans’ ability and willingness to spend. We wrote:

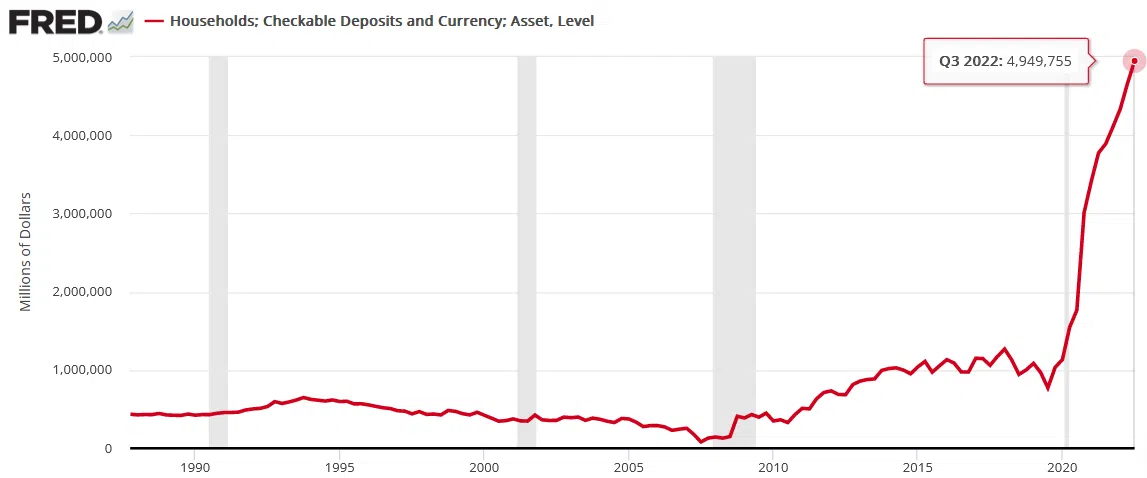

While “the Fed is trapped” crew cites these issues as reasons for an economic calamity, they often miss the forest through the trees. For example, while the fiscal spending spree may end, U.S. households are still flush with cash…. U.S. households have nearly $3.54 trillion in their checking accounts. For context, this is 253% more than Q4 2019 (pre-COVID-19).

Yet, while the FFR has surged in 2022 and the crowd still assumes that demand will collapse, the Fed revealed on Dec. 9 that U.S. households have a record ~$4.95 trillion (as of Q3 2022) in their checking and/or demand deposit accounts, which is 379% more than Q4 2019 and 6.3% more than Q2 2022.

Please see below:

Consequently, while investors wait for a destitute consumer to reduce inflation and allow the Fed to pivot, the vertical ascent on the right side of the chart above highlights the profound stimulus imbalance that materialized during the pandemic; and with wage growth also near an all-time high, investors are kidding themselves if they think monetary policy can return to its pre-pandemic state when Americans’ checking account balances have gone parabolic.

Overall, the silver price remains well above its fundamental value, as misguided inflation optimism has created hopes for a dovish pivot. Moreover, while today’s headline CPI print may be relatively weak due to the drop in oil prices, the underlying pressures remain.

Likewise, with Americans' cash balances at a record high, while the U.S. unemployment rate is near a record low, history shows that lower inflation occurs alongside economic distress and large spikes in unemployment.

Therefore, with job openings and Americans' employment expectations far from these levels, the U.S. economy, the S&P 500 and the silver price should suffer immense weakness before inflation is finally defeated.

Alex Demolitor

Precious Metals Strategist