The white metal’s narrow trading range signals a sharp move could be on the horizon.

With the pivot narrative and re-accelerating MoM inflation poised to collide in the months ahead, the QE bulls may suffer a crisis of confidence. Moreover, with QE beneficiaries like silver likely to feel the pain as the drama unfolds, the medium-term outlook is profoundly bearish.

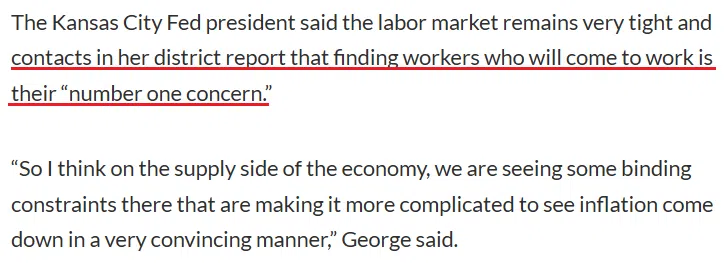

For example, while Kansas City Fed President Esther George often leans dovish, she said on Jan. 20:

“Inflation is still well above the Fed’s target. To be true to the price stability mandate, it looks like we’ll have to be a little more patient to see if we’re on the right trend and going to be there more convincingly to that 2% target.”

Thus, with labor demand still outweighing supply, she noted that it will be difficult to normalize inflation unless the imbalance is rectified.

Please see below:

Source: MarketWatch

Source: MarketWatch

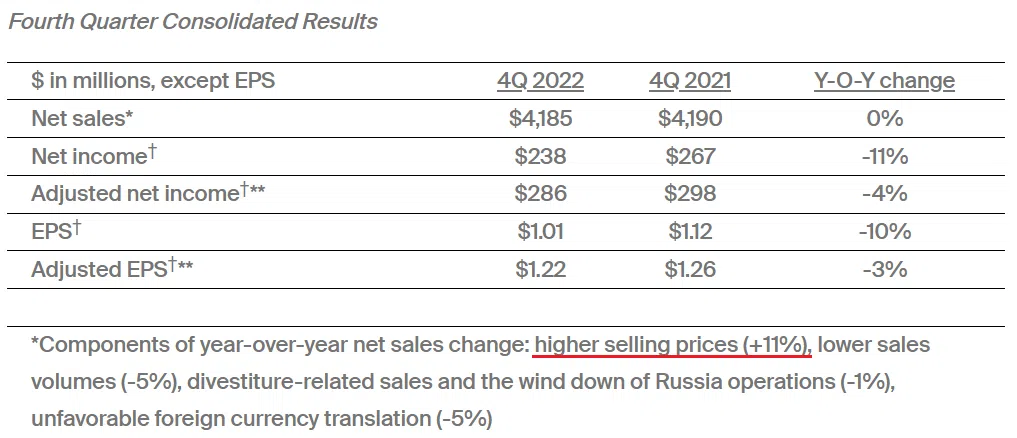

To that point, PPG Industries – a global supplier of paints, coatings and specialty materials – released its fourth-quarter earnings on Jan. 19.

COO Tim Knavish said during the Q4 earnings call that there is “significant inflation outside of raw materials,” and CFO Vince Morales added, “that's why we're doing targeted pricing across our portfolio to compensate for this other inflation that's going to be higher YoY, primarily labor.”

Furthermore, while we warned that wage inflation is the canary in the coal mine, Knavish said that higher prices will be the consequence in Q1:

“We still have pricing momentum. You know, we will have additional price in Q1 targeted by business. We've got some carryover impact in Q1 as well. You know, as for what's happening out there in the world besides PPG, you know, all the coatings companies are facing the same inflation inputs that we are.”

As a result, PPG Industries is an S&P 500 company with more than $4 billion in quarterly net sales, and it raised its selling prices by 11% in Q4; and with labor costs cited as the primary culprit – because shipping costs have plunged and commodity prices dipped – the data highlights why the crowd underestimates the peak FFR.

Please see below:

Source: PPG Industries

Source: PPG Industries

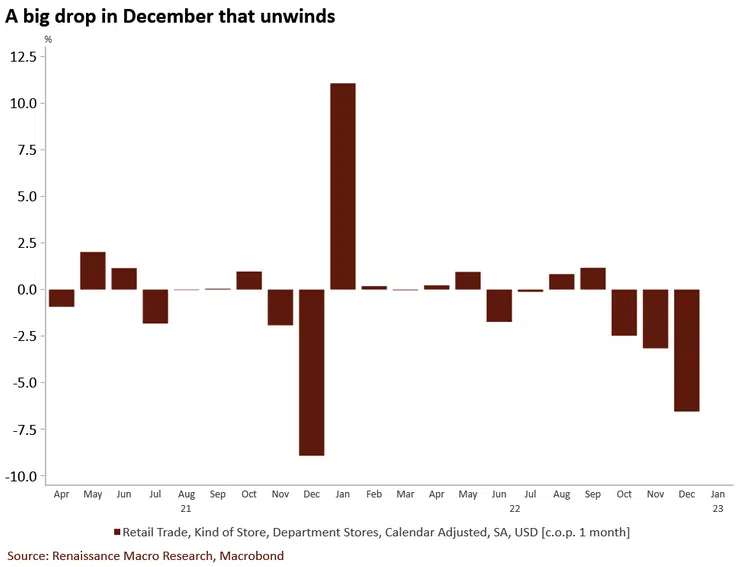

In addition, while the crowd assumes that demand destruction is near, the MoM weakness in December’s retail sales was also present in 2021. To explain, we wrote on Dec. 19:

To explain, U.S. retail sales came in weaker than expected on Jan. 18, and the brown bars on the right side of the chart above show a sharp MoM) deceleration in department store retail sales

Yet, if you analyze the middle of the chart, you can see that while sharp pullbacks were present in November and December 2021 (combined), the weakness reversed materially in January 2022; and while seasonal adjustments often skew the data, the current weakness should show a bullish reversal in the months ahead.

Likewise, with the pivot predictors missing the forest through the trees, consumers’ resiliency was on full display throughout 2022.

Please see below:

To explain, the blue bars above track the annual percentage change in U.S. retail & food services sales. Excluding 2021, U.S. retail sales posted their largest annual gain since 2004. So, while we warned repeatedly that record-high household checkable deposits and near-record-high wage inflation would keep consumer spending uplifted, little has changed.

As further evidence, Mastercard released its SpendingPulse U.S. retail sales report on Jan. 16; and relative to December 2021, the results were constructive.

Please see below:

Source: Mastercard

Source: Mastercard

Thus, while it may sound like a broken record, we have been consistent in our thesis that the fundamentals do not support a dovish pivot; and with the data still signaling higher interest rates, the demand destruction prophecies are much more semblance than substance.

In reality, consumers are still flush with cash, and wage inflation for lower-income cohorts is now running ahead of the CPI. As a result, more rate hikes, not less, should dominate the headlines before this bear market ends.

Overall, the pivot narrative is still prevalent, so the silver price remains uplifted. But, sellers continue to rush for the exits near $24, and as the momentum weakens, the inflation backdrop has turned more hawkish. Consequently, it’s likely only a matter of time before a profound pullback occurs.

Do you think the FFR will surpass 5%? Or, will demand destruction arrive sooner? Why should the Fed pivot when companies are still raising their prices and consumer spending is resilient?

Alex Demolitor

Precious Metals Strategist