The country that buys roughly one-eighth of the world's silver has thrown a licensing gate across its own import channel, and the timing explains why.

Six weeks ago, the story out of India was about a door opening. On April 1, I wrote about how India's market regulator had cleared the way for domestic mutual funds to hold physical silver, and what that institutional access could mean for a market already running short of metal.

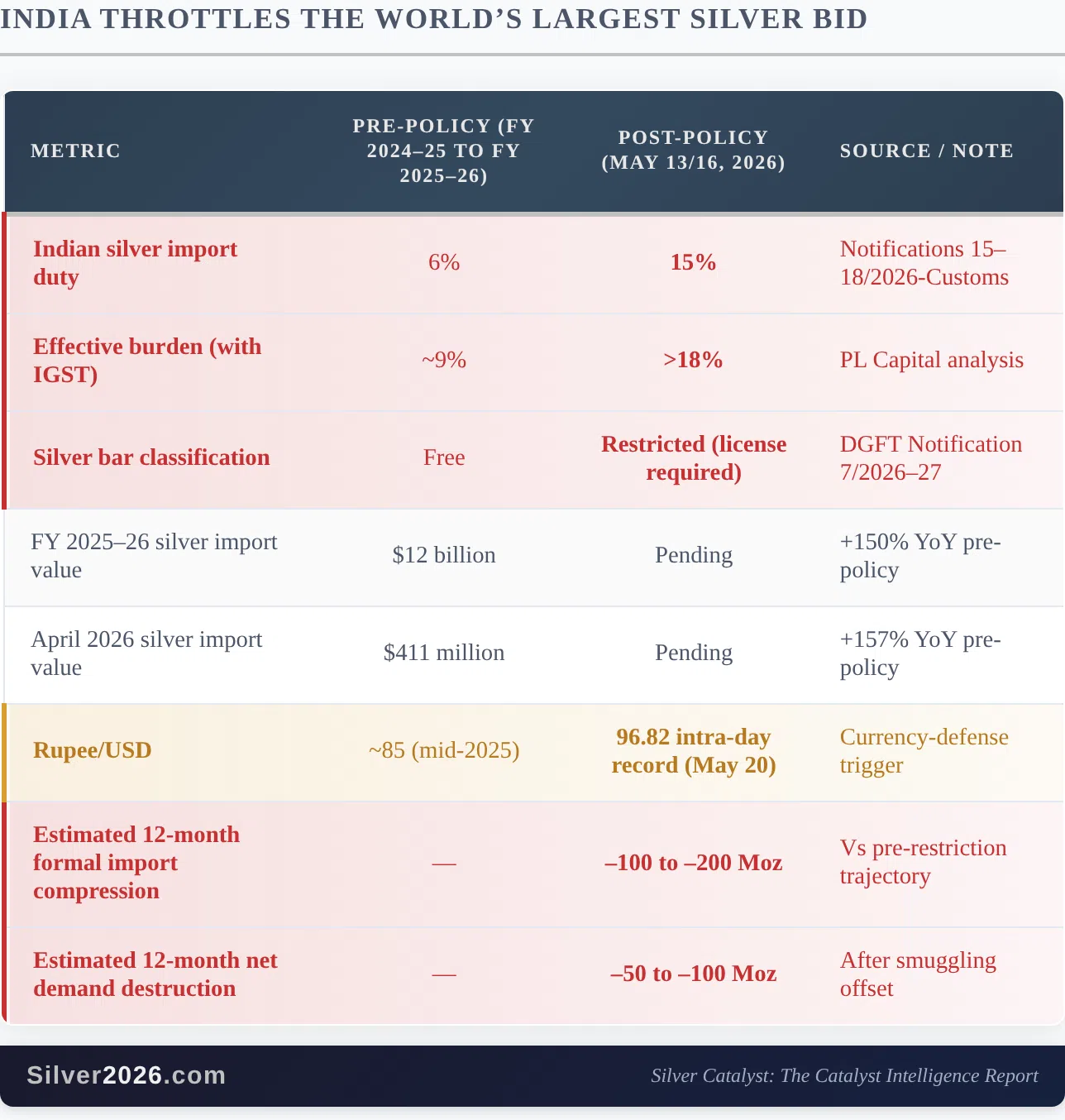

The story today is the opposite. On May 13, India raised import duties on gold and silver from 6% to 15%, and three days later it reclassified investment-grade silver bars from "Free" to "Restricted," forcing more than 90% of the country's formal silver imports into a discretionary government licensing regime. The same nation that was widening its appetite for silver in April spent the middle of May building a gate in front of it.

That reversal is not a contradiction. It is a currency-defense move, and understanding why India did it (and what it does to the silver balance) is one of the most significant demand-side developments of the year so far.

Silver, for its part, did not celebrate the supply-side implications. It fell. Fifteen days after Issue #15, the metal trades near $75.30, having given back roughly $10 an ounce across the window and dropping 2.7% on May 27 alone to an intraday low of $74.11. That decline was driven by a hawkish Fed repricing and a 10-year Treasury yield touching 4.54%, its highest in nearly a year, not by anything happening in the physical market. The gap between what the price is doing and what the fundamentals are doing is exactly the kind of divergence worth paying attention to.

There are 8 Deep Dives that I'm discussing in this week's premium Silver Catalyst issue, and in this article, I'll focus on one of them.

India Throttles the World's Largest Silver Bid

Start with why this matters before getting into the mechanics. India is the world's largest discretionary buyer of physical silver bars and coins, accounting for roughly one-eighth of global silver demand, and inside the country retail-investment demand runs structurally above industrial demand. India relies on imports for over 85% of its silver supply, since domestic mine production is essentially zero and recycling provides only the residual. When the formal import channel into a market that size gets throttled, one of the very few demand sources large enough to absorb 200 million-plus ounces of physical metal a year at the margin comes partly offline. Indian buying has historically been the demand floor that turns surplus years into balanced ones and balanced years into deficits, which is why a change to its import rules ripples through the entire global balance.

The trigger was the rupee. On May 20 the currency plunged to an intra-day record low of 96.82 against the dollar, pressured by the Iran-war energy shock, a widening current account gap, and a surge in precious-metals imports at exactly the wrong moment. India had been running roughly $12 billion in silver imports for the 2025-26 fiscal year, with volumes up 42% year over year, while importing 60% of its cooking gas and a large share of its crude. Every dollar spent importing silver was a dollar of foreign-exchange pressure the central bank could not afford during a currency crisis. So New Delhi did what governments under currency stress have done for centuries: it moved to stem the outflow.

The mechanics arrived in two waves. First, customs notifications dated May 12 and effective May 13 reinstated a 10% Basic Customs Duty plus a 5% Agriculture Infrastructure and Development Cess, with an additional 3% IGST pushing the effective burden above 18%. Then, on May 16, the Directorate General of Foreign Trade reclassified silver bars under two specific tariff codes from "Free" to "Restricted," meaning every shipment of investment-grade bars now requires a government license that the commerce ministry can grant, delay, or refuse at its discretion. The India Bullion and Jewellers Association responded by urging jewellers to stop bullion trading and limit sales to five grams or less. Two days before the duty hike, Prime Minister Modi had gone on national television asking citizens to pause non-essential gold purchases for a year to conserve foreign exchange.

The mechanism is not new, and that is the point. The previous 15% duty regime was scrapped in July 2024 precisely because it had generated systematic smuggling, which the cut to 6% had largely eliminated. Reinstating it overnight rebuilds the same incentive structure. A Mumbai bullion dealer quoted in the coverage put it plainly, warning that grey markets are likely to become active because the incentives to bring metal in illegally are now high again. So the question is not whether the duty suppresses formal imports (it will), but how much of that suppressed volume disappears versus how much simply reroutes through unofficial channels.

Here is how the displacement breaks down.

A 9-percentage-point duty hike combined with a licensing gate typically produces a 15-30% suppression of formal imports in the first quarter after implementation, with smuggling recovering 40-60% of the lost volume over the following 6-12 months. Combining those factors, the net 12-month effect plausibly compresses formal Indian silver imports by 100-200 million ounces against the pre-restriction trajectory, with perhaps 50-100 million ounces of demand actually destroyed rather than merely channel-shifted over the next two quarters. Those figures are scenario midpoints, not reported forecasts, and the honest framing matters here: a large share of the lost formal volume reappears through grey-market flows, deferred purchases, and substitution toward lower-purity feedstock that the affected tariff codes do not cover.

For context on the scale, the World Silver Survey 2026 projects global coin and net bar demand rising 18% this year to a three-year high of 257.6 million ounces, with India a major contributor: Indian physical investment grew 33% in 2025 to 79.2 million ounces, the largest of any single country. A policy that throttles the world's largest physical-investment market, just as global demand is forecast to climb, is not a footnote, even allowing for the share that reroutes rather than disappears.

There is a subtlety worth holding onto, though, because it cuts against a simple bullish read. The restriction is concentrated in investment-grade bars. Industrial silver demand routed through compounds, sputter targets, and electronic-grade granules sits largely outside the affected codes, which means the industrial side of Indian demand may prove materially more resilient than the headline numbers suggest. This is a blow aimed at the investment channel, and that is precisely where it will land hardest.

What makes the development genuinely significant is what it signals about the playbook. This validates Catalyst #12: Resource Nationalism Wave Restricting Exports and Catalyst #99: Emerging Market Currency Diversification Accelerating from "Silver Rising," and it connects directly to Catalyst #100: Currency Crisis Contagion Driving Emerging Market Silver Demand. India has established a template. Rather than burning through foreign-exchange reserves to defend the rupee, it throttled precious-metals flows directly, a cheaper and faster lever. The rupee was not alone in the window: the Turkish lira hit fresh dollar lows in the same stretch. If currency stress spreads across emerging markets and other governments reach for the same lever, the near-term effect suppresses formal demand, but the underlying driver, Catalyst #62: Currency Debasement Acceleration Patterns, is one of the most durable bullish forces in the framework. People reaching for silver because their currency is failing do not stop wanting it; they are simply told, for now, that they cannot buy it through the front door.

And that brings the analysis back to Catalyst #72: India's Cultural Silver Affinity and Demographic Explosion. India's structural demand thesis (a middle class on track for over a billion people by 2047, deep cultural attachment to physical metal, household holdings measured in tens of thousands of tonnes) does not vanish because of a licensing notification. That demand is deferred, not destroyed. The gate can be closed today and reopened the moment the rupee stabilizes, at which point the deferred buying tends to return.

What This Means

The cleanest way to read the India move is to separate the near term from the structural picture, because they point in opposite directions.

Near term, this is a genuine demand headwind, and it would be dishonest to pretend otherwise. The world's largest physical-silver buyer just made it harder and more expensive to import metal, and some portion of that demand will simply not happen over the next two quarters. Combined with the May 27 selloff to $74.11, which came from the jump in rate expectations described above rather than from anything in the physical market, the path of least resistance for the price in the coming weeks is not obviously higher. If you have followed the silver price analysis through 2025 and 2026, you have seen this pattern before: a real demand or positioning shock knocks the price, and the financial press declares the silver story over.

Structurally, the move is something closer to a confirmation. A country does not throw a licensing gate in front of a commodity its citizens do not want. India restricted silver imports because demand was surging at precisely the moment the currency could least afford it, and the duty regime it reinstated is the same one that bred a thriving smuggling trade just two years ago. The hunger is still there. It is being redirected, deferred, and partially driven underground, but it is not being extinguished. When the rupee finds a floor and the gate reopens, the deferred demand has a way of compounding.

That is the tension at the heart of this market right now. The price is reflecting a rate-channel washout and a demand-side shock. The fundamentals beneath it (a sixth consecutive structural deficit, supply that cannot respond to higher prices, and an investment-demand base that governments are now actively trying to suppress because it is too strong) point somewhere else entirely. That gap between price and fundamentals is the foundation of my longer-term price forecast, and gaps like it do not stay open forever.

The India story is one dimension of the 100-catalyst framework I analyze in "Silver Rising," alongside the seven other Deep Dives in this issue. If you want to understand where this market is headed, I encourage you to get "Silver Rising" with complimentary access to the Silver Catalyst newsletter.

Thank you.

The Silver Engineer