Peak hawkishness has the silver price riding high.

While investors are eager to turn the page on 2022, the fundamental issues that plagued the white metal haven't abated. Conversely, the coming New Year has elicited hopes of a more prosperous outcome, with disinflation and a more dovish Fed viewed as catalysts for further gains.

Yet, we've warned repeatedly that a major decline in U.S. GDP growth and the labor market are required for a dovish 180; and with economic output revised higher twice in Q3, and tracking north of 3% in Q4, the fundamental backdrop supports higher, not lower, interest rates.

Also, with resilient employment still far from the levels required to normalize wage inflation, continued hiring only strengthens the case for a higher FFR in 2023.

For example, S&P Global released its U.S. Composite PMI on Dec. 16; and while the headline index declined from 46.4 in November to 44.6 in December, the report stated:

“Private sector hiring remained subdued in December. Employment rose only marginally as manufacturers signaled broadly unchanged workforce numbers on the month and service sector hiring slipped lower to register only a modest gain.”

Remember, while the results are far from celebratory, modest employment gains are bullish for the FFR because the Fed needs employment to contract to reduce wage inflation. In contrast, U.S. firms are still increasing their headcount, which intensifies the imbalance between labor demand and supply.

Consequently, it’s no wonder why the Atlanta Fed’s Wage Growth Tracker and the U.S. Bureau of Labor Statistics' (BLS) average hourly earnings metric both re-accelerated in November; and the longer this persists, the more it supports a higher peak FFR.

In addition, the New York Fed released its Empire State Manufacturing Survey on Dec. 15. The headline index decreased from 4.5 in November to -11.2 in December. However, an excerpt read:

“Despite the overall decline in activity, the index for number of employees edged up to 14.0, marking another month of employment gains…. The pace of price increases was little changed, with the prices paid index holding steady at 50.5 and the prices received index remaining similar to last month’s level at 25.2.”

As a result, while inflation held steady, employment increased alongside intentions for future capital spending.

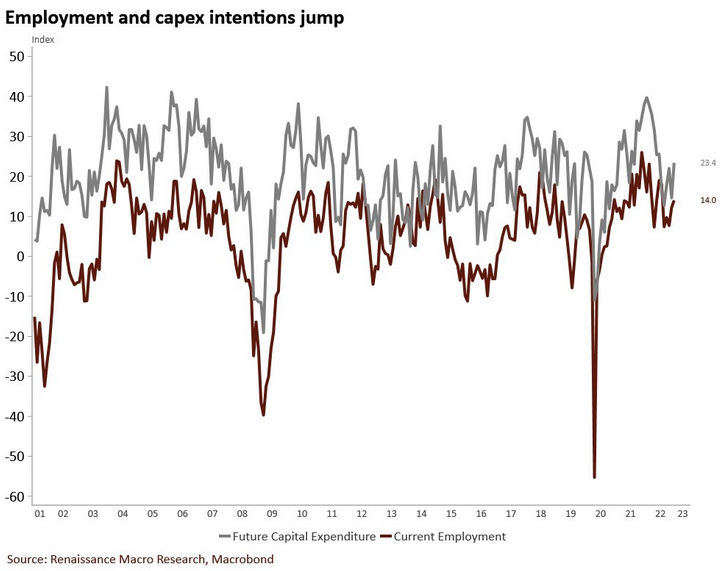

Please see below:

To explain, the brown line above tracks the New York Fed’s employment index, while the gray line above tracks the expectations index for future capital expenditures. If you analyze the right side of the chart, you can see that both metrics rose in December and are far from the troughs set during the 2001, 2008 and 2020 recessions.

For context, capital expenditures are investments in plant, property and equipment (PP&E) with a shelf life of more than one year. Furthermore, companies do not expand their cap-ex spending if they expect demand to fall off a cliff.

Also noteworthy, the Philadelphia Fed released its Manufacturing Business Outlook Survey on Dec. 15. The headline index increased from -19.8 in November to -13.8 in December. Moreover, while the inflation and employment indexes both declined, this month's “special questions” were highly revealing.

For example, the results showed that Philadelphia manufacturers are producing more now than in Q4 2021.

Please see below:

Source: Philadelphia Fed

Source: Philadelphia Fed

To explain, when respondents were asked to contrast their current capacity utilization rate with Q4 2021, the median figure increased from 70%-80% to 80%-90% (the red box above).

For context, the rate measures Philadelphia manufacturers’ actual output as a percentage of their potential output; and with more firms ramping up production in 2022, their operations have increased YoY. Likewise, with the current figure still below 100%, there is more room for future growth in the months ahead. As a result, the Fed’s 17 25 basis point rate hikes in 2022 have not capsized demand enough to reduce inflation.

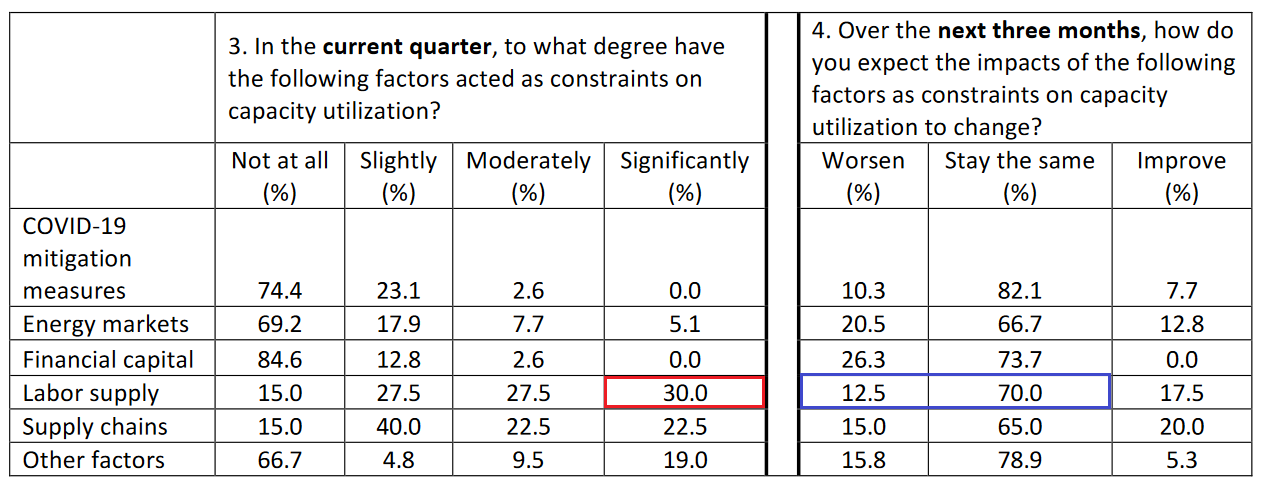

As further evidence, when asked about why their firms are operating below 100% capacity, a lack of labor supply was the primary driver.

Please see below:

Source: Philadelphia Fed

Source: Philadelphia Fed

To explain, the red box above shows that 30% of respondents cited labor supply as a significant constraint to their capacity utilization. Moreover, a consolidated 85% labeled it a slight, moderate or significant problem.

In addition, the blue box above shows that 82.5% of respondents expect the problem to remain constant or worsen over the next three months. Consequently, the findings are bullish for wage inflation, and highlight how these firms could increase their revenues if more employees were available. Therefore, the data continues to support our medium-term fundamental outlook.

But, what does all of this have to do with silver?

Well, the trajectory of wage inflation will impact the FFR. With Americans’ checking account balances at unprecedented record highs, the supply/demand imbalance in the U.S. labor market only enhances their spending power; and as long as consumers remain resilient, the lack of demand destruction will keep wage and output inflation from normalizing.

Remember, ~70% of the U.S. economy is driven by consumer spending; and when companies are fighting for employees to meet demand, the Fed will continue to see unwanted economic strength, and the FFR will need to rise much higher.

Overall, the silver price has decoupled from the fundamentals, as the crowd assumes a pivot is a done deal in 2023. Although, the data contrasts that narrative, and investors should be surprised by the lengths the Fed has to go to win its inflation fight. So, while the S&P 500 may consolidate in the short term, profound declines should confront risk assets over the medium term.

Alex Demolitor

Precious Metals Strategist