Despite the prevailing narrative, QE is much further away than silver thinks.

With profound imbalances still far from settled, the financial markets have chosen hope over reality. Moreover, while a major recession could create an economic malaise in late 2023, the current environment supports higher, not lower interest rates.

For example, Indeed released its 2023 U.S. Labor Market Outlook report on Jan. 12. An excerpt read:

“The U.S. labor market entered this year with considerable strength. Demand for workers is strong but moderating, suggesting employers are looking to add more headcount despite recession fears.”

Please see below:

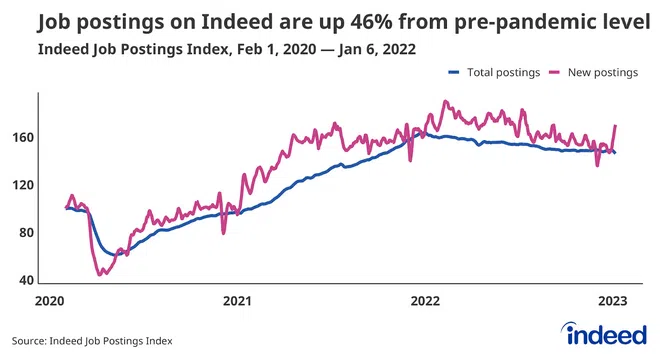

To explain, the blue line above shows that U.S. job postings on Indeed are still 46% above their pre-pandemic baseline, which highlights the resiliency of the U.S. economy. Likewise, the purple line above shows that new job postings on the site remain elevated and rose materially at the end of 2022. Therefore, the implications for labor demand and wage inflation continue to unfold as expected.

The report added:

“The experience of the Leisure and Hospitality and Retail Trade sectors is instructive. Workers in these sectors were in high demand. Leveraging that advantage, these employees realized fast wage gains and increased access to other forms of compensation….

“Their ability to quit a job and move to a new one is still sending strong signals. We will keep an eye on this metric to see how powerful these workers will become in 2023.”

Please see below:

To explain, the blue and purple lines above show how quit rates among leisure & hospitality and retail employees have increased recently after leveling off for much of 2022; and please note, Americans don’t quit their jobs unless they are financially stable or have better positions lined up. Consequently, the data is bullish for wage inflation.

On top of that, while Indeed noted that “the increases slowed near the last half of 2022… employers [are] advertising benefits at a higher rate than in the past.”

Please see below:

To explain, the blue, purple, and brown lines above show that job postings on Indeed that include health, paid time off, and retirement benefits continue to hit new highs. So, if demand destruction was present, employers would not be offering extra incentives plus higher wages to attract talent, and that’s why the crowd underestimates the ultimate peak of the U.S. federal funds rate (FFR).

Speaking of which, while investors price in a lower peak FFR than the FOMC and subsequent rate cuts in 2023, Philadelphia Fed President Patrick Harker said on Jan. 12:

“I expect that we will raise rates a few more times this year, though, to my mind, the days of us raising them 75 basis points at a time have surely passed. In my view, hikes of 25 basis points will be appropriate going forward.”

As a result, while 25 basis points may seem relatively dovish, please remember that higher interest rates are hawkish no matter the increment. Moreover, even if the Fed raises the FFR to 5% and holds it there in 2023, the outcome is still more hawkish than what’s priced in.

Please see below:

Source: Bloomberg

Source: Bloomberg

Likewise, while we’ve noted the performance of the Atlanta Fed’s Sticky CPIs and their implications for broad-based inflation, Richmond Fed President Thomas Barkin said on Jan. 12:

“I would caution that while the average dropped, the median stayed high. That’s because the average was distorted by declining prices for goods like used cars that escalated unsustainably during the pandemic.

“If the center of the [CPI] distribution remains above our target, then I think we should continue to move rates. Inflation is going to be more persistent than a simple drop down to 2%.”

Making three of a kind, St. Louis Fed President James Bullard said on Jan. 12:

“There's probably too much optimism inflation is going to easily come back to 2%. That is not the history of inflation. We are really moving into an era of higher nominal interest rates for quite a while going forward as we try to continue to put downward pressure.”

As such, while the crowd expects rate cuts in the months ahead, the fundamentals and the Fed’s messaging support a materially different outcome.

Please see below:

Source: MarketWatch

Source: MarketWatch

In addition, with the U.S. 10-Year real yield often peaking alongside the FFR, continued rate increases are bullish for one of silver’s main fundamental adversaries. To explain, we wrote on Jan. 10:

With the U.S. 10-Year real yield hitting a 2022 high of 1.74% and ending the Jan. 9 session at 1.31%, a rise above 2% is well within the expected range of outcomes. Furthermore, if the FFR surpasses the YoY core CPI like it has in every inflation fight since 1961, the U.S. 10-Year real yield could hit 2.5% or more. Either way, the current market pricings contrast the historical and economic realities required to normalize inflation.

Finally, with investors’ optimism poised to be their downfall, the loosening of financial conditions makes it even more likely that inflation will stay uplifted for longer than the consensus expects.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the red line above tracks the FFR’s upper bound, while the blue line above tracks the Goldman Sachs Financial Conditions Index (FCI). If you analyze the right side of the chart, you can see that the FCI has fallen below its December lows, which only makes the Fed’s job more difficult.

Therefore, if the divergence continues, the stimulative effect undermines the Fed’s current progress and lessens the impact of any future progress. As a result, investors’ expectations contrast with the environment needed to win this inflation battle.

Overall, the silver price remains well above its fundamental value, as we believe the days of pre-pandemic monetary policy are long gone. Moreover, with a sharp contraction of economic activity likely needed to normalize inflation, a major sell-off of the S&P 500 should materialize in the months ahead; and with silver hitting its 2022 lows alongside the S&P 500 in September and October, the correlation should prove ominous once again.

What do you think? Does the FCI move higher in H1 2023? Why is the consensus playing chicken with the Fed? Who do you see emerging victorious?

Alex Demolitor

Precious Metals Strategist