While Brent crude surged 50% in ten days, silver sat quietly at $84 — coiled on top of the worst COMEX delivery crisis in exchange history.

Oil crossed $100 a barrel on March 9 for the first time since 2022, then kept going, briefly touching $119.50 before settling around $108. The Strait of Hormuz, through which 20% of the world's oil flows, has been effectively closed since the US and Israel launched strikes against Iran on February 28. Kuwait, Iraq, and the UAE are cutting production because they've run out of storage. The new Supreme Leader, Mojtaba Khamenei (the slain leader's son and an IRGC hardliner) was elected on March 8. Nobody is talking about a ceasefire.

Normally, this would dominate every financial headline. And it does — for oil, for equities, for bonds.

But for silver, there's a different story. Silver is trading at $82-85, consolidating quietly after its $96.40 spike on March 2. The February correction, which took silver from its $121.64 all-time high to a $64.14 intraday low, wiped out 90% of managed money positions. The speculative froth is gone. What remains is physical demand, and the numbers are extraordinary.

In Issue #7, I documented how the January-February crash revealed the widest paper-physical divergence in decades. In Issue #8, I tracked the COMEX inventory decline below 90 million ounces and the BHP-Wheaton $4.3 billion streaming deal. Now, the convergence of war, delivery stress, and industrial demand has created conditions I described as theoretically possible in "Silver Rising", but didn't expect to see activated simultaneously.

There are nine Deep Dives in this week's premium Silver Catalyst issue, and in this free article, I'll discuss three of them.

War With Iran and the Oil-Silver Transmission Mechanism

On February 28, the United States and Israel launched coordinated military strikes against Iran. The strikes killed Supreme Leader Ali Khamenei. Within days, Iran retaliated by effectively closing the Strait of Hormuz, cutting off approximately 20% of global oil transit. By Day 10 of the conflict, CENTCOM had struck more than 3,000 targets and destroyed 43 Iranian warships. Over 1,332 Iranians have been killed. Seven US service members have died. Hezbollah re-entered the conflict on March 2. A US submarine sank an Iranian warship on March 4, the first submarine combat sinking since the Falklands War.

The oil response tells the severity. Brent crude surged approximately 10-13% on the initial March 2 reaction. By Friday March 7, it had risen 28% for the week, the largest weekly gain since April 2020. On March 9, it surged past $100 and briefly touched approximately $119.50 before pulling back to around $108 after G7 finance ministers began discussing a coordinated strategic petroleum reserve release. The cumulative oil shock from pre-war levels now exceeds 50%.

Silver spiked to $96.40 intraday on March 2 before retreating. Gold surged to $5,417 on March 3. But while gold's response was sustained, silver's was violent and brief, which is characteristic of a market where thin positioning creates liquidity vacuums that amplify both spikes and pullbacks.

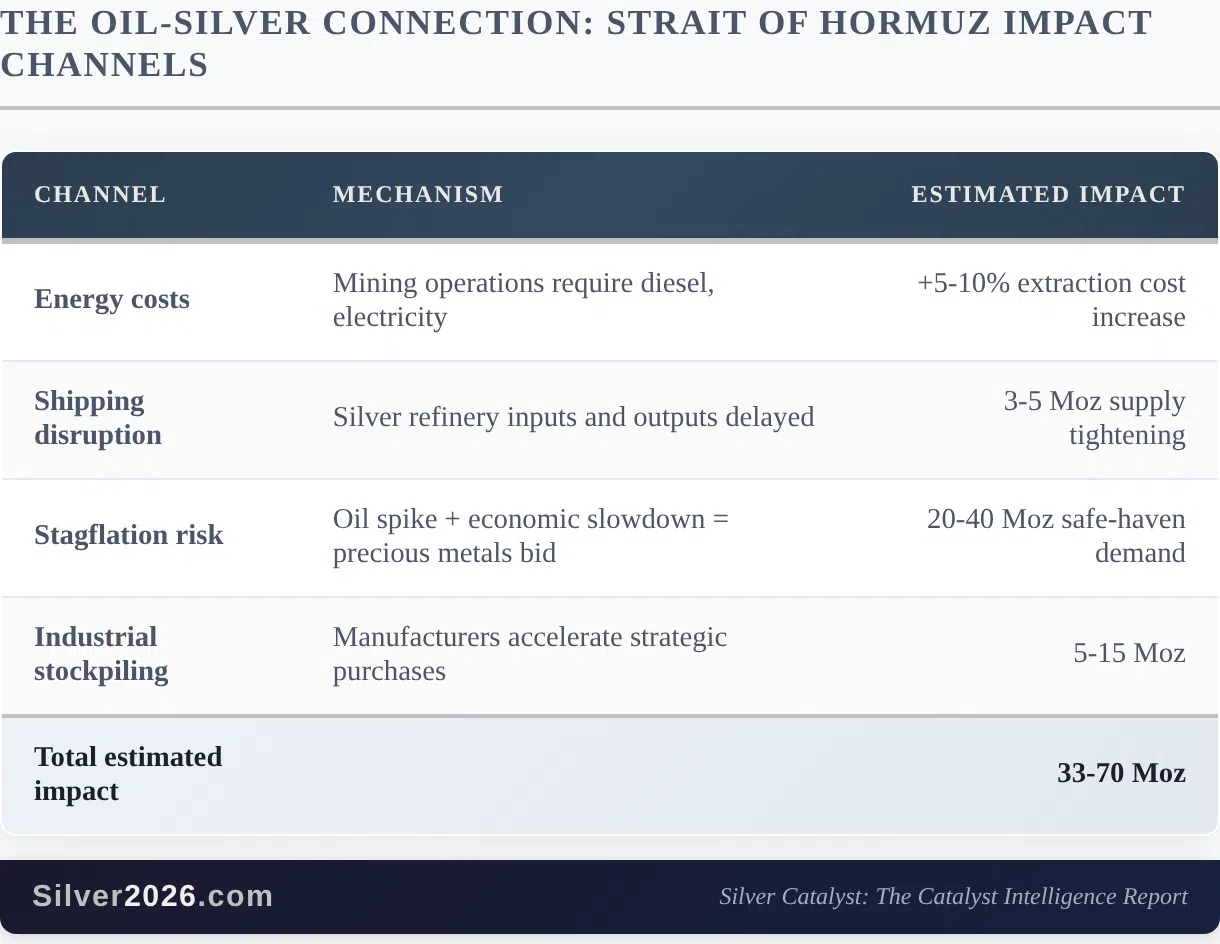

How Oil Translates Into Silver Demand

The Hormuz closure affects silver through multiple channels. I calibrated these estimates against three historical precedents: the 1973 oil embargo, the 1979 Iranian Revolution, and the 2019 Aramco drone attack.

The total estimated impact of 33-70 Moz equals roughly half to the entirety of the projected 2026 structural deficit of 67 Moz, from this single geopolitical event alone.

The election of Mojtaba Khamenei as Supreme Leader on March 8 makes this more structural than temporary. He's a hardliner with deep IRGC ties. Trump demands "unconditional surrender." Israel has threatened to target any successor. The longer this war persists, the more the safe-haven demand component hardens into permanent demand embedded in the 2026 deficit.

COMEX Delivery Crisis: 59% of Registered Inventory Demanded in One Month

While the Iran war dominates headlines, the COMEX silver delivery crisis is quietly reaching a breaking point.

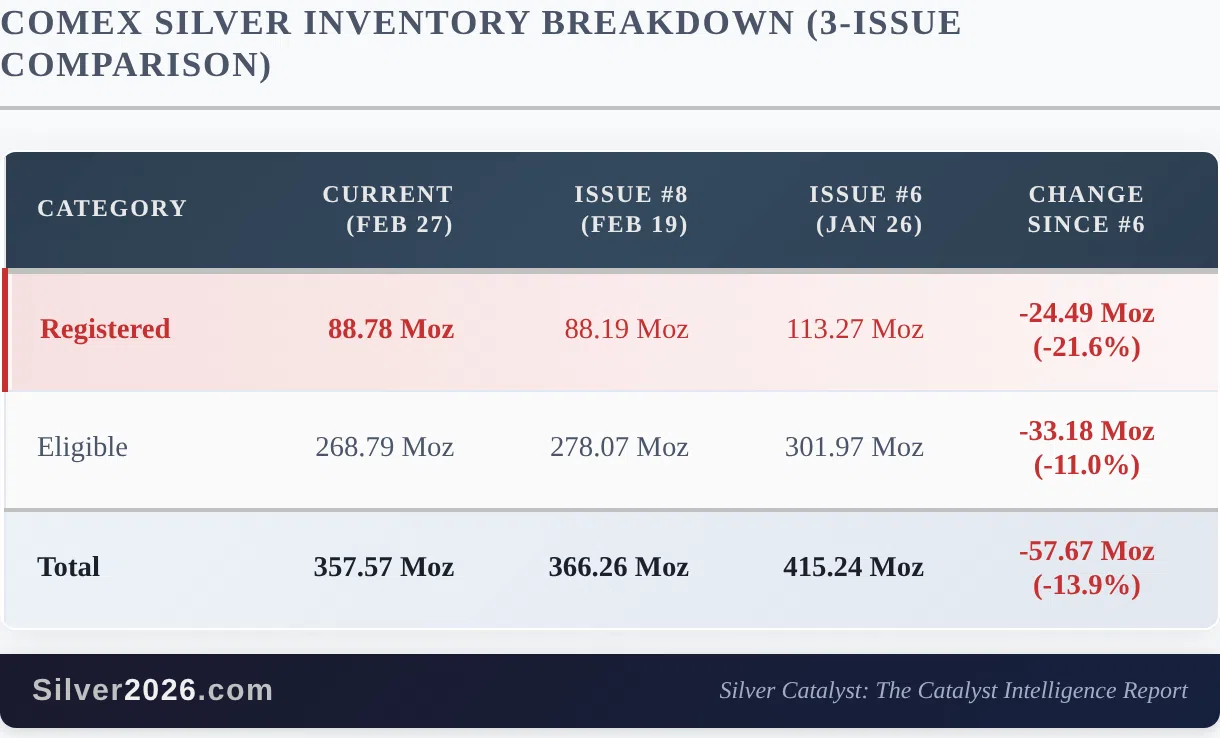

On March First Notice Day, 10,526 contracts stood for delivery, representing 52.63 million ounces of physical silver demand. COMEX registered inventory (the metal actually available for delivery) stands at 88.78 Moz. That means 59.3% of all registered silver is being demanded in a single delivery month.

February was already extraordinary. A total of 5,036 contracts (25.18 Moz) were physically delivered, the highest February figure in modern COMEX history. Combined with January's deliveries, approximately 75 Moz was delivered out of COMEX vaults in just 60 days, which is roughly 85% of the current registered inventory turned over in two months.

Registered inventory has fallen 64% from the April 2020 peak of approximately 240 Moz. The pace is accelerating. And unlike what economic theory predicts, higher prices aren't attracting metal back into vaults — they're draining it faster.

This creates a binary outcome for COMEX. Either the exchange honors the deliveries with physical metal, draining inventory toward dangerously low levels. Or it forces cash settlements, exposing the gap between paper claims and actual metal. Either way, the outcome is bullish for silver.

If you've been following the silver price analysis throughout 2025 and 2026, this dynamic has been building for months. The January-February paper crash that I analyzed in the Issue #7 free article didn't solve the delivery problem, but rather accelerated it. Physical buyers treated the crash as a buying opportunity, and COMEX drainage continued without interruption.

AI's $700 Billion Silver Appetite

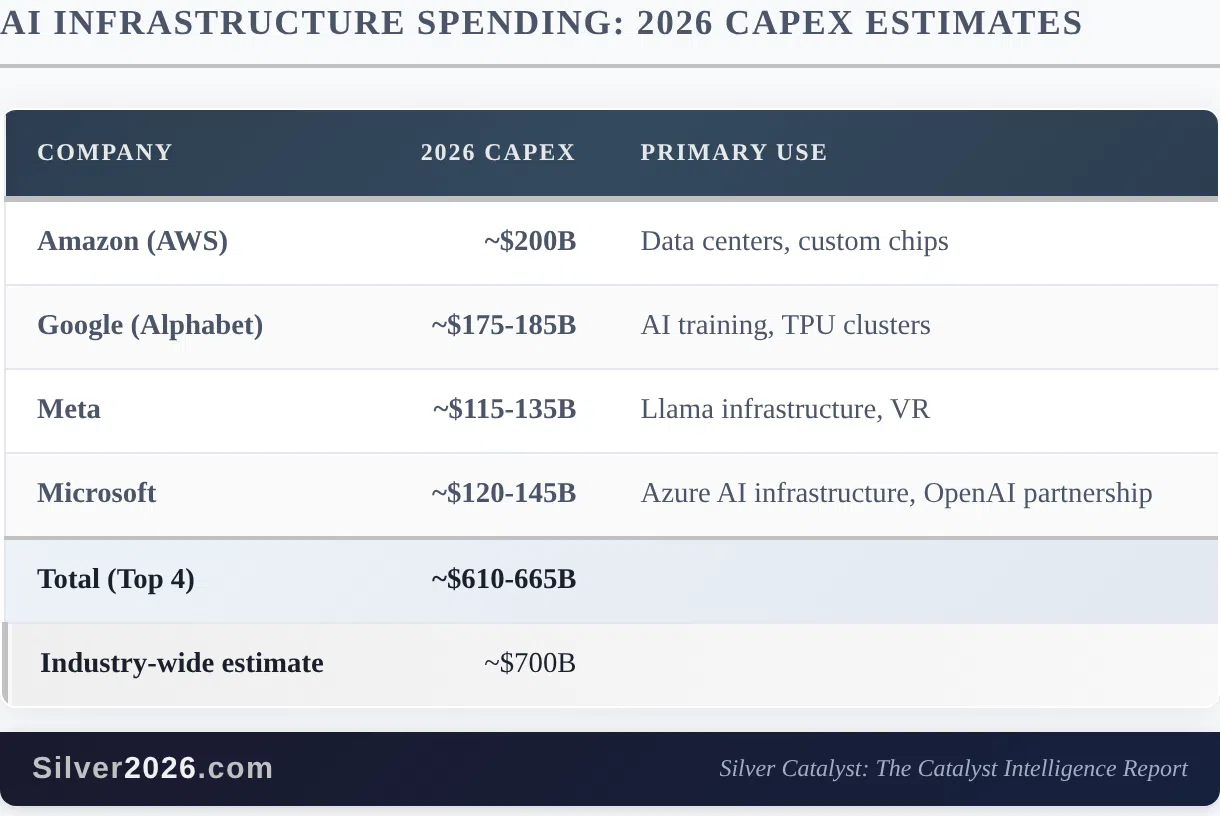

The third force worth examining has nothing to do with war or COMEX. It's the scale of AI infrastructure spending.

Goldman Sachs projects that data center power demand will increase 165% by 2030. Every one of those data centers requires silver in thousands of applications: server electrical contacts, high-frequency cables and connectors, thermal interface materials, power distribution systems, and electromagnetic shielding. Unlike solar panels, where silver thrifting is reducing per-unit consumption, data center applications have no commercially viable substitute for high-frequency electrical contacts and thermal management.

My estimate, derived by scaling silver intensity per gigawatt of installed IT capacity against Goldman Sachs' projection of approximately 50 GW installed in 2025 growing to approximately 122 GW by 2030, is that AI and data center infrastructure consumes 60-80 Moz of silver annually and is growing. That would make it the third-largest category of silver industrial demand after solar and electronics.

There's a compounding factor that most analysts miss. The global memory chip shortage is projected to persist through at least late 2027, with virtually all available high-bandwidth memory capacity allocated to AI. Each chip requires silver in die-attach materials and wire bonding. The bottleneck simultaneously constrains AI deployment speed while ensuring sustained silver demand from the semiconductor supply chain.

This demand is price-inelastic. When you're spending $200 billion on a data center, the silver content is a rounding error. AI infrastructure builders won't reduce silver consumption because the price rose from $30 to $85. They'll pay whatever it costs.

What This Means

Three forces — geopolitical disruption, physical market stress, and industrial demand — are converging on a market with 88 million registered ounces and a sixth consecutive structural deficit.

The Iran war is not a silver-specific event, but it amplifies every other driver simultaneously. Higher oil raises mining costs for an industry that already can't increase output at $80+ silver. Shipping disruptions tighten a market already in deficit. Stagflation fears drive investment demand at the exact moment managed money positioning is at its lowest in years. And industrial consumers, watching supply chains fracture in real time, are stockpiling.

Meanwhile, COMEX is being asked to deliver 53 million ounces in March against 89 million registered. AI infrastructure is consuming 60-80 Moz annually and growing. India's mutual fund industry gains access to silver allocation on April 1, which is 23 days from now. And China's export controls, now in their 68th day, continue to fragment global supply.

The February correction shook out every speculative long. It didn't resolve a single fundamental imbalance. If anything, lower prices encouraged more physical accumulation, exactly the dynamic that has characterized this market since 2021.

Silver at $84 is not reflecting the fundamental reality beneath it. It's reflecting the aftermath of a positioning washout. That gap between price and fundamentals doesn't persist indefinitely. Something has to give.

The convergence I just described is one dimension of the 100-catalyst framework I analyze in "Silver Rising." The full Issue #9 contains six more Deep Dives covering China's export controls and the two-front supply squeeze, the broken mining supply response, India's SEBI reform and its potential to unlock 34-168 Moz of new demand, the stagflation case and the Fed's impossible position, market structure stress including the CME trading halt and Eric Sprott's $300 projection, and solid-state battery progress with the EU Digital Product Passport. If you want to understand where this market is headed and stay informed as it unfolds, I encourage you to get "Silver Rising" with complimentary 2-week access to the Silver Catalyst newsletter.

Thank you.

The Silver Engineer