Four major primary silver producers just filed their Q1 results. Three reported falling output and cited the same cause. Silver is at $75 today. The ore grades don't care.

Silver is trading at approximately $75.69 this morning, down from $87 on May 14. The drop was sharp: over 10% on May 15 alone, triggered by April PPI data showing the steepest single-month producer price spike since early 2022, which effectively erased any remaining market expectation of a Federal Reserve rate cut this year. UBS added to the pressure, slashing its full-year silver investment demand forecast and cutting its deficit estimate. The selloff was real, and the reasons behind it were real.

What did not change is the supply side.

Four major primary silver producers filed their Q1 2026 production results in the past two weeks. Three of the four reported declining output, all citing the same structural cause, and none described it as temporary. At the same time, the most recent COMEX warehouse report, filed May 18, shows registered silver at 80.91 Moz, essentially unchanged from the 79.88 Moz reported in early May, with total inventory at 315.15 Moz. The physical silver available for delivery at COMEX has not materially changed in either direction. The market has moved. The supply picture has not.

In the May 13 issue of Silver Catalyst, we covered six structural developments across the silver market. In this article, I'll focus on one of them.

Three Miners, One Problem, No Short-Term Fix

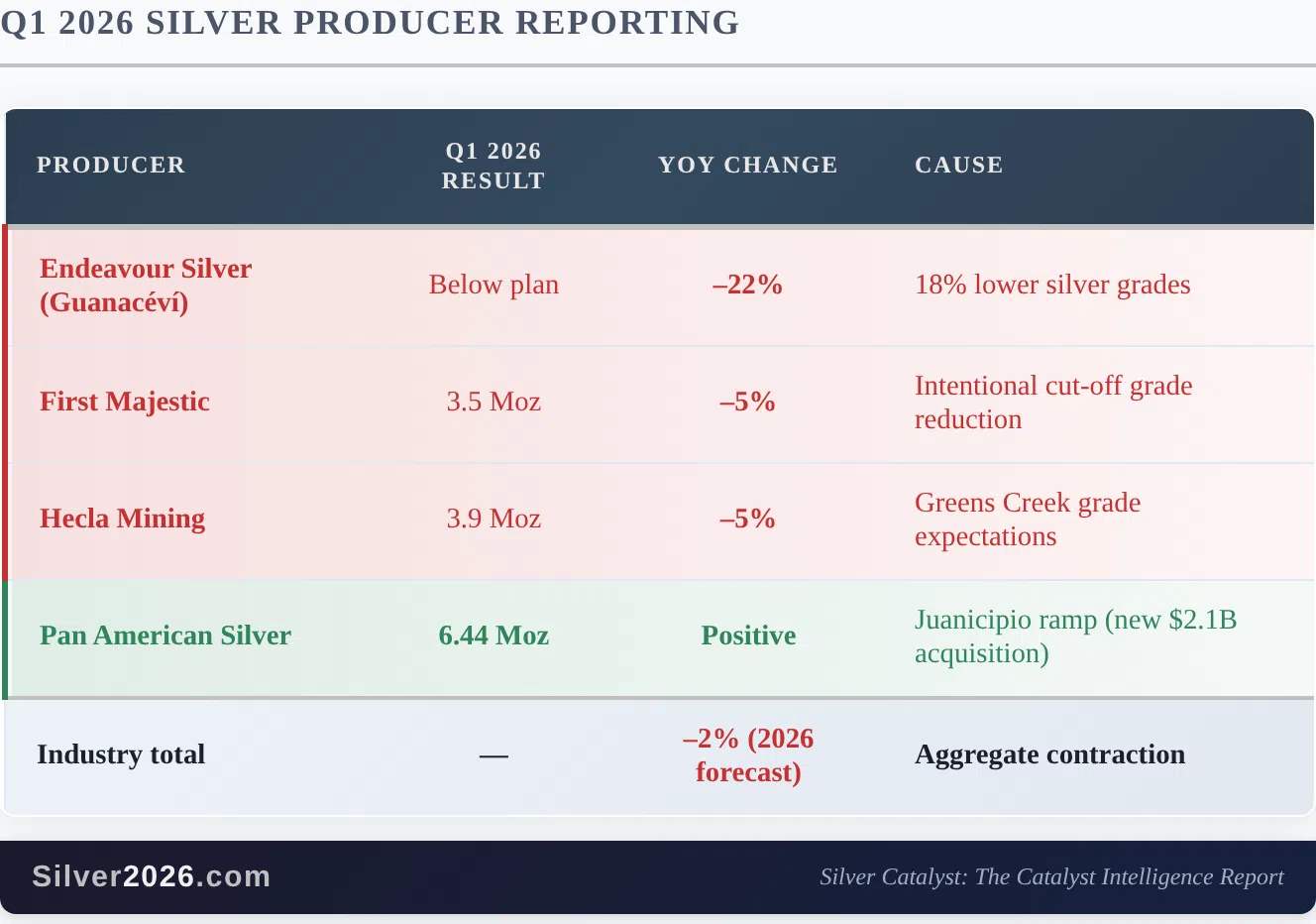

The Q1 2026 production reports from the world's major silver miners are in, and three of the four filed so far show the same pattern: output down, driven by falling ore grades that the companies themselves describe as structural rather than temporary.

Endeavour Silver reported production at its core Guanaceví mine down 22% year-over-year, attributing the decline directly to "18 percent lower silver grades," meaning the ore body itself contains less silver per tonne than it did a year ago, not that the mine is running below capacity. That distinction matters: a higher silver price can make it worth processing marginal rock, but it cannot put higher-grade ore where none exists. First Majestic illustrated the same dynamic from the other direction, reporting a 5% decline (3.5 Moz versus 3.7 Moz in Q1 2025) while disclosing it is now deliberately processing lower-grade rock it previously would have left in the ground; the higher price has already pulled forward the marginal ore, leaving less high-grade material for future quarters. Hecla reported production 5% lower at 3.9 Moz and reaffirmed guidance already reflecting a step down from 2025's 17 Moz output, driven by grade expectations at its main Greens Creek mine.

The one exception is Pan American Silver, which produced 6.44 Moz in Q1 at a cost of just $6.63 per ounce and reaffirmed its 25.0–27.0 Moz annual guidance. The reason Pan American is bucking the trend is that it acquired MAG Silver's stake in Mexico's Juanicipio mine last year, adding an entirely new asset that is ramping up cleanly. That kind of uplift requires acquiring or building a new mine, at enormous cost and over many years. It is not something most producers are doing, and it is not something that a price move in either direction can accelerate.

The industry-wide picture, per Metals Focus and the Silver Institute, is a 2% contraction in total silver supply in 2026, against a backdrop of the sixth consecutive annual market deficit.

Why a Lower Silver Price Makes This Worse, Not Better

The price drop this week does not help the supply problem. It makes it worse. Here is the mechanism.

When silver was trading near $87, marginal mines and lower-grade ore bodies were borderline viable. At $75, some of that marginal production is no longer economic. The mines do not respond to a price drop by increasing output to compensate; they respond by curtailing production of their lowest-grade material. The supply contraction that Metals Focus and the Silver Institute forecast at 2% for 2026 was calculated at higher price assumptions. A sustained period at $75 could produce a larger contraction than the current consensus estimates.

Meanwhile, the industrial demand that drives roughly 60% of silver consumption does not respond to a 10% price move in the way that investment demand does. Solar panel manufacturers, electronics producers, and electric vehicle supply chains procure silver on the basis of manufacturing schedules and contract terms, not daily spot prices. The demand does not disappear when the price falls.

What does change with a price drop is the investment premium. At $75, silver sits approximately 38% below its January 29 all-time high of $121.67 and is trading near the level it occupied at the start of Issue #14 on April 28. The silverpriceforecast.com analysis throughout 2026 has treated the structural supply deficit as the foundation of the bull case. That foundation has not changed. The silver price analysis documented the ore grade problem before this week's reports confirmed it across three producers simultaneously.

Catalyst connections:

- Catalyst #5 (Ore Grade Decline Creating Exponential Cost Increases): validated in Q1 disclosures at Endeavour (Guanaceví), First Majestic, and Hecla simultaneously; the structural condition is now documented at the producer-reporting level, not just the theoretical level.

- Catalyst #13 (Planned Mine Closures by 2030): with 2% supply contraction forecast for 2026 and no significant new projects offsetting the trajectory, the supply picture is moving in one direction. A price drop to $75 does not reverse it.

The Context

Silver at $75 is not evidence that the investment thesis is broken. It is evidence that macro factors (in this case a PPI-driven rate-hike scare and a UBS demand forecast revision) can override structural fundamentals in the short term. That has happened before and will happen again.

What the Q1 producer reports do is provide a concrete, company-filed, audited data point showing that the supply side is moving in exactly the direction the catalyst framework predicted. Three major producers reported simultaneously declining grades. None described it as temporary. The Juanicipio ramp at Pan American is real but exceptional, and it required a $2.1 billion acquisition to achieve.

The full Silver Catalyst Issue #15, built on the framework in Silver Rising, covers five more developments from the same two-week window: silver's 16-to-1 outperformance of gold on May 11 and what the ratio compression from 62.25 to 55.46 means; the most divided Fed vote in 34 years and three historical precedents for what happens to silver when the central bank is paralysed; the Glencore Kazzinc explosion in Kazakhstan that put 3.4 Moz of byproduct silver at acute risk; Gold Fields' first quantification of Iran-war oil costs at $40 to $50 per ounce AISC impact; and the April CPI stagflation reading. If you want to stay informed as this market develops, I encourage you to get "Silver Rising" with complimentary 2-week access to the Silver Catalyst newsletter.

Thank you.

The Silver Engineer