Is the divergence from Jan. 4 a cause for concern?

Despite the recent enthusiasm surrounding the PMs, silver was a noticeable underperformer on Jan. 4; and with the S&P 500 ending the day in the green, the white metal’s decline was even more noteworthy. Thus, while one day doesn’t make a trend, silver’s fundamentals are tracking in the same bearish direction as gold.

For example, the FOMC released the minutes from its Dec. 13-14 monetary policy meeting on Jan. 4; and with the revelations highly hawkish, the PMs are ignoring the developments at their own peril. An excerpt read:

“Participants reaffirmed their strong commitment to returning inflation to the Committee's 2 percent objective. A number of participants emphasized that it would be important to clearly communicate that a slowing in the pace of rate increases was not an indication of any weakening of the Committee's resolve to achieve its price-stability goal or a judgment that inflation was already on a persistent downward path.”

In addition:

“Several participants commented that the medians of participants' assessments for the appropriate path of the federal funds rate in the Summary of Economic Projections, which tracked notably above market-based measures of policy rate expectations, underscored the Committee's strong commitment to returning inflation to its 2 percent goal.”

On top of that:

“With inflation still elevated, the staff continued to view the risks to the inflation projection as skewed to the upside….

“Some participants also noted that, by some measures, firms' markups were still elevated and that a continued subdued expansion in aggregate demand would likely be needed to reduce remaining upward pressure on inflation.”

So, while the FOMC emphasized its “resolve to achieve its price-stability goal,” and noted that its peak FFR estimate “tracked notably above market-based measures of policy rate expectations,” investors still assume the FOMC is bluffing.

However, we’ve noted repeatedly that the fundamentals support higher interest rates, and the post-GFC crowd should learn this lesson the hard way over the medium term.

To that point, the FOMC minutes added:

Source: U.S. Fed

Source: U.S. Fed

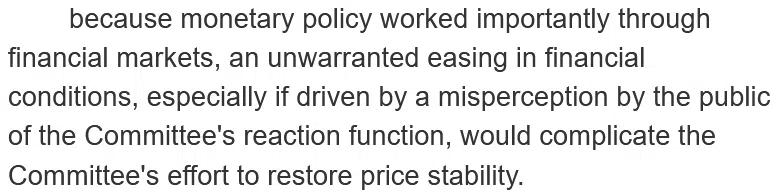

Therefore, while the silver price has benefited from “a misperception by the public of the Committee’s reaction function,” we warned on Dec. 15 that looser financial conditions were antithetical to the FOMC’s goals. We wrote:

Higher stock prices, lower interest rates, a weaker U.S. dollar and smaller credit spreads support inflation and make the Fed's job harder. Again, that's why investors' hopes for a dovish pivot actually reduce the chances of one occurring.

The more the markets dissent, the more inflation will reign, and the higher the Fed will need to push the FFR. As a result, don't be surprised if economic reality haunts the pivot bulls in the months ahead.

To that point, while the PMs have largely ignored the ramifications, the FOMC’s battle against an “unwarranted easing in financial conditions” should materially shift sentiment over the medium term.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the black line above tracks Goldman Sachs U.S. Financial Conditions Index (FCI). If you analyze the middle of the chart, you can see that the deceleration from mid-October to mid-December is the opposite of what the Fed wants; so unsurprisingly, the FOMC reversed this narrative on Dec. 14, and the rising black line on the right side of the chart highlights how the fundamentals continue to align with our expectations.

Thus, we expect the FCI, the USD Index and the U.S. 10-Year real yield to hit new highs in 2023. Remember, higher values for all three help alleviate inflation, and the crowd is uninformed about what it will take to permanently reduce the pricing pressures.

Finally, as mining stocks print lower highs versus the S&P 500, please note that silver is highly volatile and exudes similar characteristics; and since we see a sharp slide in the S&P 500 in 2023, silver and mining stocks should suffer the brunt of the devastation.

Moreover, with Satori Fund Manager Dan Niles highlighting the S&P 500’s disdain for inflation on Jan. 3, the PMs are unlikely to celebrate if the S&P 500 comes under pressure. He wrote:

“We believe that reductions in S&P earnings estimates and further multiple compression will drive the next market move lower….

“We think the estimate for CY23 will eventually be closer to $200 from its peak of $252 when looking at earnings reductions during prior recessions. In 2022 these estimate cuts led to drops in the stock market and we believe the same will hold for 2023.

“Our single point price target for the market bottom on the S&P is 3,000 derived from 2023 S&P EPS of $200 with a 15x multiple. At the low end we can see the S&P reach 2,400 based on a 12x multiple which is not unreasonable at inflation levels above 5% historically.”

Please see below:

Source: danniles.com

Source: danniles.com

Overall, silver exudes the same misguided optimism that drove its other bear market rallies in 2022. Yet, when investors' pivot hopes crashed, the silver price followed suit. As such, while the bulls remain loyal to their post-GFC playbook, we believe the game has changed, and the dip buyers should suffer more pain before it's all said and done.

Alex Demolitor

Precious Metals Strategist