Trump says Iran talks are in "final stages." WTI crude fell 5.7% to $98.26 yesterday. Silver climbed above $76 on the news. The mechanism behind that move is worth understanding.

The silver market has been following the Iran war since the day it started in late February. When oil spikes on escalation, mine operating costs rise and inflationary pressure pushes the Fed to hold rates, which is bad for silver. When peace signals emerge, oil falls, costs ease and rate-cut expectations return, which is good for silver. On Wednesday, silver climbed above $76 after Trump said a US-Iran deal was in its "final stages," with oil falling more than 5% on the same news.

WTI dropped below $100 after Trump's comments. Adding to the market reaction, ship tracking data showed a South Korean supertanker carrying Kuwaiti crude and two Chinese supertankers crossing the Strait of Hormuz on Wednesday, in what may be some of the highest-volume tanker traffic through the strait since the war began. This is not a settled outcome yet. Trump has made similar optimistic statements before, and key sticking points remain including Iran's nuclear programme and Hormuz access. The move in silver is not pricing in a completed deal; it is removing some of the war premium.

In the May 13 Silver Catalyst issue, we covered this exact mechanism in a Deep Dive on Iran-war mining input costs. In this article, I'll look at the other side: what an end to the war, or even a sustained de-escalation, actually means for silver.

The War Premium in Oil, and Where It Lives in the Silver Supply Chain

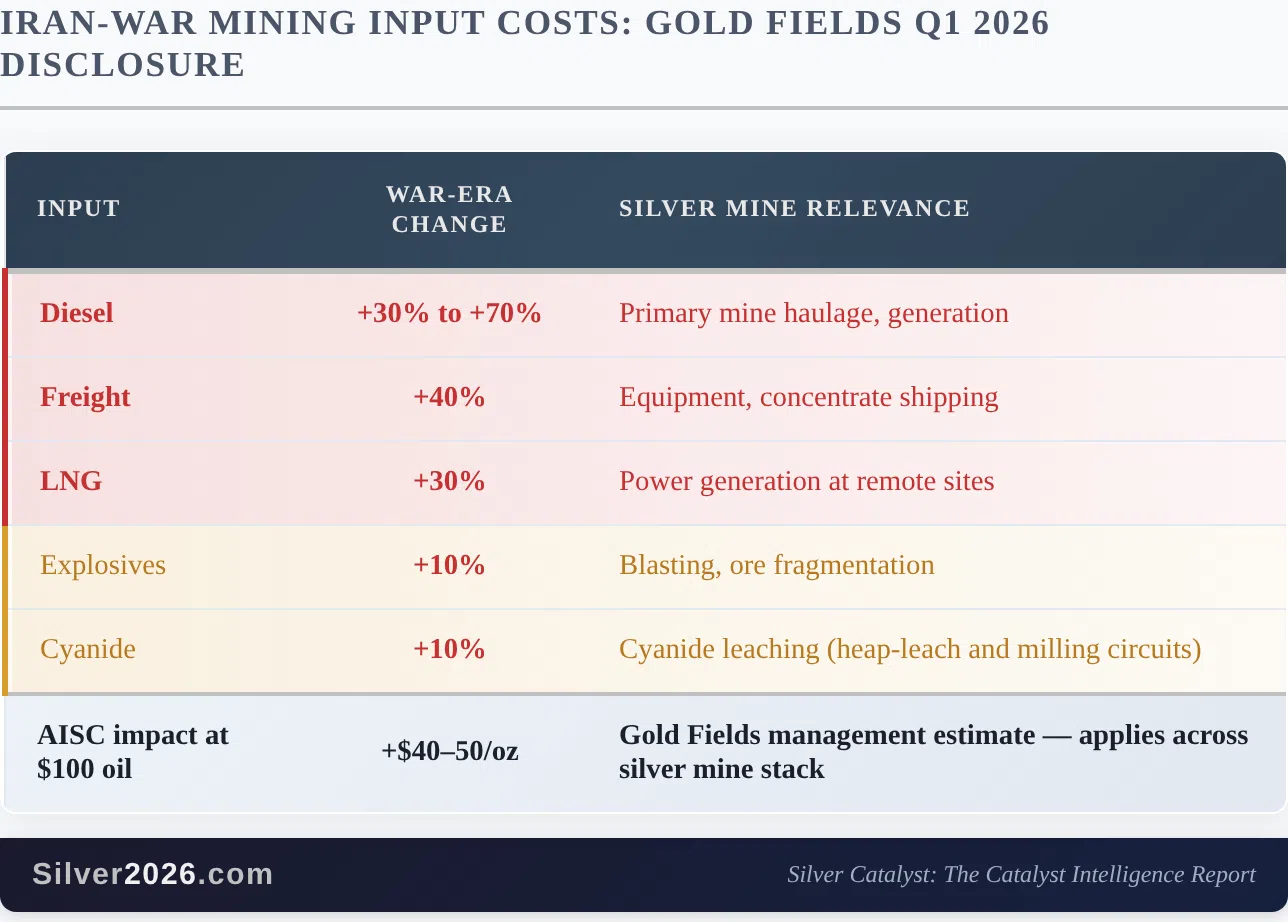

The Iran war added a structural premium to oil that runs through the silver supply chain in ways that are not immediately obvious. In its Q1 2026 results, Gold Fields became the first major miner to quantify the damage: diesel costs up 30 to 70%, freight up 40%, LNG up 30%, with management estimating a $40 to $50 per ounce all-in sustaining cost impact at $100 oil. Those inputs apply equally to silver mines.

That cost shock did not happen in isolation. It arrived on top of the ore grade decline that three major silver producers (Endeavour Silver, First Majestic, and Hecla) all reported simultaneously in their Q1 results: production down 5 to 22%, driven by grade declines of up to 18%, with none of them describing the condition as temporary. The combination of structural grade decline and war-driven cost inflation created a supply picture that was compressing from both sides at once.

Wood Mackenzie has estimated that if the US and Iran reach a deal that opens the Strait of Hormuz by June, Brent prices could ease to around $80 per barrel by end-2026. That is not a guaranteed outcome, and most analysts remain cautious. Despite the signs of progress, supply tightness would likely persist even if a deal were concluded, since supply will likely not return to pre-war levels immediately. But even a partial unwind of the war premium matters for the mining cost stack.

Why Lower Oil Is Silver-Positive on Two Separate Channels

The first channel is direct: lower diesel, freight, and LNG costs reduce the all-in cost of producing silver. Mines that were marginal at $75 silver and $104 oil become more viable at $75 silver and $85 oil. The supply contraction that Metals Focus and the Silver Institute are forecasting at 2% for 2026 was calculated against elevated energy cost assumptions. A sustained oil price decline would ease, though not eliminate, that pressure.

The second channel is the Federal Reserve. The April CPI reading of 3.8% was driven substantially by energy, with energy contributing +17.9% year-over-year to that number. If WTI settles sustainably below $90, the energy component of CPI reverses, and the Fed's paralysis (the inability to cut without stoking inflation, or hike without choking growth) eases on one side. The June CME FedWatch probability for a rate cut has been near zero for most of May, with the market pricing the Fed firmly on hold through the summer. Wednesday's oil drop is beginning to shift that: some forecasters now put June cut odds as high as 28% if the Iran deal holds and energy prices continue falling. A sustained decline toward $85 to $90 WTI would move those probabilities meaningfully, which would be directly bullish for silver.

What the Gold-Silver Ratio Is Saying Today

The previous article on this topic covered the ratio compression from 62.25 to 55.46 in thirteen days, with silver outperforming gold 16-to-1 on May 11 as the Trump-Xi summit approached. That compression has since partially reversed. The ratio today sits near 59.5, having widened from its May 11 low as silver gave back more of its gains than gold after the PPI-driven selloff on May 15.

A ratio of 59.5 is still well above the 47 to 50 historical norm. At current gold prices near $4,490, closing that gap to 50 implies silver near $90. The ratio at 59.5 also means silver is cheap relative to gold compared to where it was on May 11, the same setup that preceded the May 11 rally, not a deteriorating one.

The COMEX picture has not materially changed: the latest warehouse report filed May 20 shows registered silver at 81.67 Moz, up marginally from 79.88 Moz in early May but essentially flat in a market that has seen the spot price drop 13% from its peak. Physical silver available for COMEX delivery has not moved meaningfully even as the paper price has fallen sharply. That divergence (price down 13%, registered inventory essentially unchanged) is a signal about where the physical bid sits.

Catalyst connections:

- Catalyst #6 (Energy Costs Amplifying Silver's Supply Inelasticity): a sustained oil price decline directly reverses the cost shock that Gold Fields quantified at $40 to $50 per ounce AISC; lower energy costs ease but do not eliminate the supply contraction trajectory.

- Catalyst #59 (Silver's Regime-Dependent Inflation Sensitivity): lower oil reduces the energy component of CPI, potentially giving the Fed room to act; the stagflation regime that is historically most bullish for silver depends on the Fed remaining paralysed, which a deal-driven oil decline could partially disrupt.

- Catalyst #67 (Safe-Haven Demand Amplification During Uncertainty): the May 7 Iran peace optimism session (+6.60%) and Wednesday's move above $76 on deal progress confirm the same mechanism; silver responds to Iran de-escalation as an industrial-demand signal, not a fear signal.

The Structural Case Does Not Need the War

The point worth separating from the Iran news cycle is this: the silver supply deficit does not require the war to persist. The sixth consecutive annual deficit at 46.3 Moz per Metals Focus and the Silver Institute is a function of industrial demand running above mine supply, a relationship that exists independently of oil prices or geopolitical risk. The ore grade decline at Endeavour, First Majestic, and Hecla does not reverse when oil falls. The Kazzinc byproduct disruption in Kazakhstan that put 3.4 Moz at risk is unrelated to Iran.

What the Iran war did was add a cost premium on top of a supply structure that was already contracting. A deal removes the premium, not the structure.

The full Silver Catalyst Issue #15 covers all six structural developments from this two-week period in detail, including the Fed paralysis, the gold-silver ratio compression, the Kazzinc explosion, the Q1 producer results, and the April CPI stagflation confirmation. If you want the complete picture as this market develops, I encourage you to get "Silver Rising" with complimentary 2-week access to the Silver Catalyst newsletter.

Thank you.

The Silver Engineer