On April 14, a Chinese battery startup backed by one of the world's largest automakers rolled the first A-sample all-solid-state battery cells off a production line in Guangzhou.

The company is targeting GWh-scale output by the end of 2026, twelve to eighteen months ahead of where Toyota's timeline stood at the start of this year. The silver market has not priced this in.

Silver is trading around $80 today, roughly 34% below the January 29 all-time high of $121.67 and within 3% of the April 17 intraday peak, recovering sharply as news broke that the US sent a one-page memorandum of understanding to Iran through Pakistani mediators, sending oil down more than 6% and easing the inflation expectations that had weighed on silver throughout April. The Fed transition is in its final days: Warsh cleared the Senate Banking Committee 13-11 on April 29, with a full Senate floor vote expected the week of May 11. None of this has altered the supply picture documented in the World Silver Survey 2026, and none of it has slowed the pace at which the technology demand side of this story keeps advancing.

Greater Bay Technology's A-Sample Changes the Timeline

Greater Bay Technology (GBT) is a battery startup backed by GAC Group, China's fourth-largest automaker by volume. On April 14, GBT confirmed that A-sample all-solid-state battery cells are now rolling off its production line in Guangzhou's Nansha district. The specifications: energy density of 260 to 500 Wh/kg (compared to roughly 250 to 350 Wh/kg for current liquid lithium-ion); stable 2C to 3C fast charging; and a proprietary deep eutectic composite electrolyte that passed needle penetration, extrusion, and thermal shock testing without thermal runaway. Vehicle integration in GAC's Hyptec models is the target platform. GWh-scale production is targeted by the end of 2026.

That last point is what changes the industry timeline.

Toyota has been the most credible name in solid-state development for the better part of a decade. Its announced target for mass production has been 2027 to 2028. GBT's April 14 announcement puts A-sample production hardware in Guangzhou now. Not in 2027. Not in a laboratory. The commercialization clock has moved.

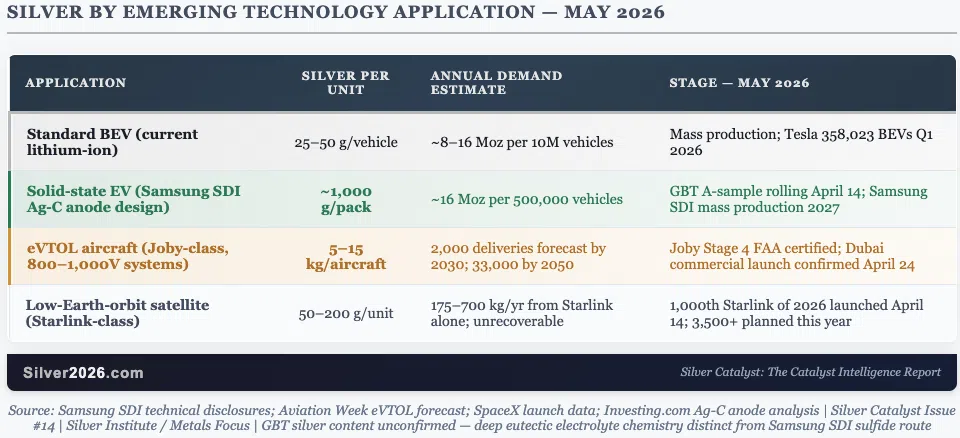

Why Solid-State Batteries Are a Silver Story

Catalyst #80: Solid-State Batteries Requiring Enhanced Silver Content in Silver Rising describes the mechanism. Samsung SDI's leading solid-state architecture uses a silver-carbon (Ag-C) composite anode, approximately 5 grams of silver per cell, and roughly 200 cells per pack, producing around 1 kilogram of silver per 100 kWh of battery capacity. In a mid-size EV with a 75 kWh pack, that is roughly 750 grams of silver per vehicle.

Current liquid lithium-ion EVs use between 25 and 50 grams of silver per vehicle, primarily in electrical contacts, sensors, and thermal management. Solid-state architecture at Samsung SDI's silver intensity would represent a 15x to 30x increase per vehicle in silver content.

Sources: Samsung SDI technical disclosures; Aviation Week eVTOL forecast; SpaceX launch data; Investing.com Ag-C anode analysis. Silver Catalyst Issue #14, Silver Institute / Metals Focus.

GBT has not publicly disclosed whether its deep eutectic electrolyte uses a silver-carbon anode. The chemistry is distinct from Samsung SDI's sulfide-based route. Direct silver intensity for GBT's specific design is not confirmed.

The category activation is what matters regardless of GBT's exact composition. Samsung SDI's 2027 mass production target (the most detailed public solid-state silver roadmap available) now exists in a competitive environment where GBT is already producing A-samples at scale. Competition in a category compresses timelines. The solid-state silver demand event, which forecasts pointed toward the late 2020s, is moving closer.

Three More Events From the Same Two Weeks

The GBT announcement arrived alongside three other developments from the same April 14 to 28 window, each advancing a distinct technology demand catalyst.

Tesla Cybercab. On April 23, Tesla confirmed that volume production of the Cybercab has begun at Giga Texas, the first fully autonomous vehicle model entering mass production at a major Western automaker. Tesla delivered 358,023 battery electric vehicles in Q1 2026, reclaiming the global quarterly BEV crown from BYD (310,389 units). At 25 to 50 grams of silver per current-generation BEV, Tesla's Q1 deliveries alone consumed roughly 9,000 to 18,000 kg of silver from a single manufacturer in a single quarter. As solid-state architectures enter the mix, that per-vehicle figure rises.

Joby Aviation and Uber. On April 24, Joby and Uber confirmed that air taxi service will launch in Dubai later this year, bookable directly through the Uber app at four vertiports. Joby has cleared Stage 4 of FAA type certification, with Stage 5 the final pre-commercial barrier. Catalyst #84: eVTOL Aircraft Electrical Systems describes why this matters for silver: eVTOL aircraft operate at 800 to 1,000 volts, significantly higher than the electrical systems of conventional aircraft, and require an estimated 5 to 15 kilograms of silver per aircraft for power distribution in weight-critical applications. Aviation Week forecasts 2,000 eVTOL deliveries by 2030, rising to 33,000 by 2050. The Joby-Uber Dubai launch is where the category moves from certification progress to paying passengers.

SpaceX Starlink. SpaceX launched its 1,000th Starlink satellite of 2026 on April 14 (the same day as GBT's A-sample announcement), putting the constellation on track for more than 3,500 launches this year. The total operational constellation now exceeds 10,000 satellites. Catalyst #88: Satellite Constellation Deployment Acceleration puts silver content at 50 to 200 grams per satellite for space-qualified components in a radiation-hardened environment. At 3,500 satellites per year, that is 175 to 700 kilograms of silver annually from Starlink alone; a small number in isolation, but permanent and unrecoverable, and one that grows as Amazon's Project Kuiper, China's G60/Qianfan constellation, and the European IRIS2 network each scale toward their own targets.

The Pattern Across All Four Events

None of these four events announces immediate, measurable silver consumption at a scale that moves the annual supply-demand balance on its own. What they share is something different: each one advances the timeline on a category of demand that didn't exist at meaningful scale five years ago and is projected to be material within this decade.

Solid-state EVs, autonomous vehicles, eVTOL aircraft, and satellite constellations are all categories where silver's physical properties are load-bearing, not incidental: conductivity, thermal management, resistance to oxidation in extreme environments. The same properties that make silver irreplaceable in solar cells and COMEX-grade bullion make it the material of choice when electrical systems need to be both high-performance and reliable under stress.

The silver analysis that identified this pattern before the current bull run remains intact. The demand floor isn't being built by one application. It's being built by dozens of them advancing simultaneously, with different timelines and different silver intensities, in a market where the supply side has produced essentially flat mine output despite a 42% annual average price in 2025.

The full Silver Catalyst Issue #14 covers seven additional Deep Dives: the World Silver Survey 2026 confirming the sixth consecutive annual deficit and 762 million ounces of cumulative above-ground drawdown; the Hormuz war's continued suppression of silver despite a textbook stagflation configuration; the COMEX May delivery cycle with 153 Moz in paper open interest against 77.12 Moz of registered metal ahead of First Notice Day; the solar demand reset and the Fraunhofer ISE factor-of-10 silver reduction breakthrough, with a forward trajectory through 2030; the SILVER Act and the first endorsement of vault decentralization by a sitting US precious-metals regulator; India's Akshaya Tritiya festival producing record trade growth against a silver price that has tripled in INR terms; and Fresnillo's Q1 confirming Mexico's output in a third consecutive year of structural decline. The Catalyst Dashboard, institutional price targets, and Events to Watch through July are all included. To follow this market as the technology timeline compresses, I encourage you to get Silver Rising with complimentary 2-week access to the Silver Catalyst newsletter.

Thank you.

The Silver Engineer